FUTURE IMPERFECT - November 2001

| It’s been a terrible year for

games magazines, with more closures than CTW can remember and once-major players like EMAP

seemingly unable to get out of the market fast enough. But no-one’s suffered more

than the once billion-pound-rated Future Network. Concerned shareholder Stuart Campbell

looks for both the smoking gun and the way out.

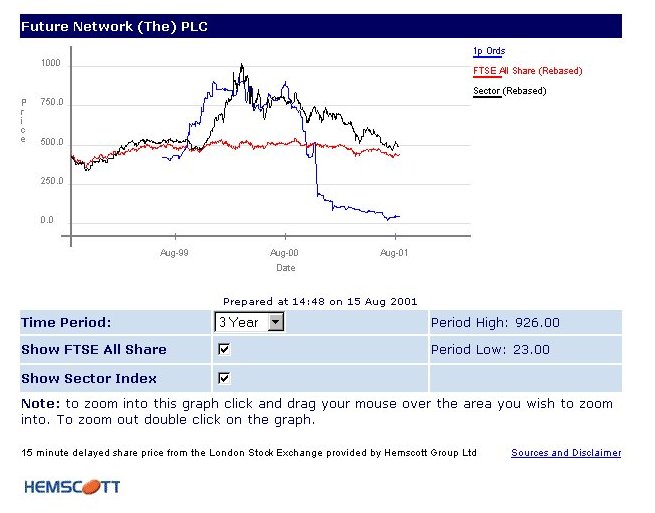

It has, it must be said, been a pretty grim year for the media in general, and not just in the videogames arena. Advertising spends are drastically down, share prices are following them, and everyone seems to have belatedly realised that the internet isn’t going to provide a major revenue stream after turning a blind eye to the total lack of a viable business model for years. Venture capitalists who were writing blank cheques 18 months ago to anyone with a website are hotfooting it away from the whole media sector like a dog from a carwash. But even in a world of nightmares, nobody’s having bad dreams more vivid than The Future Network, nee Future Publishing. Switching their brand focus towards the net just in time to get caught in the dotcom crash, the Bath-based publisher has seen its share price collapse by a breathtaking 97% over the last year or so (hugely out-plummeting the falls of the sector in general – see fig 1), fuelled by accounting irregularities, profits warnings and massive debt brought about by unwise and excessive investment as well as difficult market conditions. From a peak market capitalisation value of around Ł1.3 billion, you could now (at time of writing, the last-resort rights issue which will more than double the number of shares in the company notwithstanding) snap up every single share in TFN for a bargain Ł35 million - or somewhere roughly in the region of Ł300,000 per magazine published. (The whole company’s value is considerably less, in fact, than Time/AOL just paid for a single title, the company’s former flagship Business 2.0, which was responsible for a fifth of the firm’s total revenue last year.) The share price has continued to fall despite several drastic measures – the company shed close to a quarter of its entire workforce (throwing 500 people out of work), closed down dozens of magazines and dispensed with the services of its Managing Director, Mike Frey, and Financial Director Ian Linkins (and more recently, rather quietly, chairman and founder Chris Anderson), all without improving the City’s confidence in Future’s future - shattered as it was by that darkest of all possible events to the stock market, a series of consecutive profits warnings just weeks apart. (And of course, there have been less drastic measures too. Among the first casualties of the cutbacks were the company’s hired pot plants – I don’t know about you, readers, but the sheer senseless, impatient decadence of renting out pot plants always strikes this reporter as one of the earliest signs that a company’s lost all touch with reality.) But we know all this already. The most puzzling thing about it all, though, is that on the surface, it’s difficult to see exactly what’s changed at Future. The company is still far and away the market leader in its core business - videogames magazine publishing – and accounts for every other copy of a videogames magazine sold anywhere in the UK. The management team hasn’t changed that significantly, the way the company does business hasn’t changed any, and it’s achieved considerable growth at relatively low cost, by snapping up lots of other firms and properties with equity when that equity was still worth something. So why is a company so popular a year ago such a pariah now? The only person properly qualified to answer that question is the former editor of Amiga Format, Future’s long-serving CEO Greg Ingham. So, in a 90-minute interview at the leather-upholstered heart of the Future management bunker, I asked him. CTW: So, Greg. How on Earth did you get into this Godawful mess, then? GI: Well, firstly, if you look at the competitive landscape I wouldn’t change where we are now for anywhere we’ve been before – we’re in a better place now than previously, at any point you care to choose. CTW: Aren’t you just holding your competitive position because everyone else can’t get out of the games-magazine business quick enough? GI: Yeah, but if EMAP had had the profitability that Future has had even in this downcycle, then they wouldn’t be getting out of the market. You don’t sell from a position of strength, you sell from a position of weakness. CTW: It’s odd to hear you talking about "profitability" in the current circumstances. GI: You know, there’s any amount of - entirely understandable - complexity and misinterpretation of our numbers. The games division, and the UK business as a whole, has been profitable for many years, in terms of actual operating profit. Now, I’m not happy with the profit it’s made, and I’m not claiming that it’s a major achievement or anything of that sort – there’s still a hell of a lot of work to do. But I think the City, the analysts, and increasingly the employees here, will realise the difference between the sort of technical writeoffs we’ve had to make with goodwill and suchlike, and actual cash-in-cash-out operating profit in terms of the continuing business. CTW: So if the business is inherently profitable, and all the losses are these abstract non-cash factors like goodwill, how did you manage to land yourself with such a big cash debt that it cost you close to half your entire staff, a third of your magazines, a Managing Director and nearly the whole company? GI: Of course there have been some one-off items – the cost of closing the German business, the cost of selling Business 2.0, the cost of the redundancy programme. All of those are cash items, they’re real costs but not recurring costs. Also, debt isn’t inherently a bad thing – we all have debt in our lives. But as long as you can service that debt, and as long as the provider of the debt believes that you can service it, then it isn’t necessarily a bad thing. We had a lot of debt when we bought the company from Pearson, some of which was paid down at the flotation and some of which was paid down from profit in 1999, but we also racked up costs by acquisitions and so on, to the extent that we had a debt which in other circumstances would have been straining us, but just about manageable. Simultaneous to that, though, we had a sharp downturn, a bigger downturn than we’d been expecting in technology generally and in games peripherally. So you’ve got the big debt there at too high a level, and the ability to service the debt being much more constrained than we’d expected, and then you have the problem and you have to take action. It’s painful, bloody, horrible action that’s had to be taken, we’ve lost very good colleagues and very good friends, but having taken those tough actions, having sold B2.0 for a very good price indeed, having the rights issue and the debt facility, the business is in much better shape in terms of its capital structure than it’s been in a long, long time. CTW: What grounds do you have, in the light of the mistakes which brought about this situation in the first place, that you’re not simply going to make the same mistakes again, though? GI: Some of what happened was to do with over-reaching, an awful lot of it came about due to external circumstances – if NASDAQ goes off a cliff, if technology companies stop R&D, and manufacturing, and then advertising, and so on, the events of September 11, somewhere along the line we as a media company focused on technology are going to be hit by that. CTW: You’ve underperformed your media sector by a long way, though. You can’t blame it all on the NASDAQ and the World Trade Centre. GI: Yes, we’ve underperformed, and we’d over-performed the sector before, for much of our life as a public company until last October [This doesn’t actually seem to be the case – see Fig.1]. We came in at a very high price, significantly ahead of where virtually anyone expected us to be, and then it grew and grew. And when you have that tremendous success initially, you have the City roaring you on, you have investment in a bull market, which it then was, and we simply took on too much. That was the big mistake – it was too much to do all that in one go, and from the position of having an inappropriate capital structure, that’s where the errors were. There were micro-errors too, to do with tactics, timing, experience and so on, which we absolutely hold our hands up to, and have done through a variety of public documents and statements, but the reality is that we are where we are, and what matters is digging ourselves out of the hole that we’re in, whosoever has created that hole. And the view that shareholders have taken, through the rights issue, is that they’re going to give us another Ł35 million because they believe that we are able to have taken the actions we have and develop the value of the business going forwards. CTW: Well, the rights issue has been underwritten, that’s not quite the same as the shareholders volunteering to take it up… GI: Well, the top 16 shareholders have all committed to putting in at least the same, pro rata, as their current holdings, and some are putting in significantly more than that. CTW: There’s been a certain amount of scepticism over the directors not taking up the issue, though. Chris Anderson is selling 10 million of his shares - rather than buying the 40 million or so he’s entitled to under the rights issue – and you yourself are only taking up 100,000 of your entitlement of somewhere around 5 million. It’s not a great vote of confidence from the chairman and CEO, is it? GI: Well, I’ll speak personally – and I have to preface this by saying it’s not a recommendation to anyone else, they have to make their own judgement and so on – but my own view is that if I had the money, I would absolutely take up my allocation. As it is I’m being heavily diluted, I’m losing disproportionately from the upside that I believe will come to the business. Through a number of personal factors which I’m not going to go into, I have various commitments that I can’t get out of, and I didn’t sell my shares previously. I was bloody foolish not to sell out at five, six, seven quid, but I didn’t, and I don’t have the financial resources. Chris is in a different position, and it’s for him to speak, but this part is publicly known – he has a substantial loan outstanding, a private matter not related to our business, and in order to pay off that loan he’s selling shares. He can’t determine when that happens – if you’re in hock to someone else, it’s not for you to determine when you have to pay it off. But from a strictly personal point of view, do I think 20p is a bloody good price to buy Future shares? Absolutely I do. I think it’s a very low price. If I had the money, I’d be doing it as well. But we shall see. CTW: Do you think it was just bad luck that you chose to hitch your cart to the Internet, with the rebranding as The Future Network, just as the wheels fell off that particular wagon? Did it lead to a perception in the City that you were an Internet company and contribute to the enormous collapse in your share price, perhaps disproportionately to events? GI: It’s sort of the other way round. We had within our business an Internet business which was valued at hundreds of millions of pounds, and like most Internet businesses at the time, disproportionately valued to its revenue. There was no profit, it was just revenue. We had something like Ł6 million revenue from the Net business in 2000, yet it was valued at hundreds of millions. Then sentiment changed, although we hadn’t changed what we were doing, and that hundreds of millions became nothing. So in that respect, yes, we had a disproportionate upside then a disproportionate downside from the Internet. It’s like a souffle, or a balloon within something. A souffle inside a balloon. Or perhaps a glass gravy dish inside a steak-and-kidney pie or something. But anyway, the rebranding wasn’t a deliberate, cynical decision to try and jump on the bandwagon. We felt as though we were overlapping into that sort of area by dint of the magazines we published, and when that fell away we lost the value. CTW: In terms of going forward, are you concerned that you’ve had to offload so much of the family silver, as it were? Business 2.0 represented 20% of the entire company’s revenue, you’ve closed around a third of your entire magazine portfolio, sacked 40% of your staff, closed flagships like Daily Radar, hacked investment to the bone... Doesn’t that leave you in an unpleasant Catch 22 situation? How do you get back by launching successful new magazines when there’s nothing in the investment kitty? GI: We’ve made sure that where we’ve cut, it’s been in areas which are either larger scale, or more speculative, or less core, or sometimes all three. Where we haven’t cut is, particularly, in the games market. We know that it would be insane to nickel-and-dime where there is great opportunity and where we have the best track record. We’ve had to walk away from opportunities in other areas, we simply haven’t got the money, but we’re very protective of our games magazines – they’re the ones which will make sure we’re driving forward in the appropriate fashion. Official Playstation 2, for example, is a profitable magazine. What matters from here is managing that profitability, riding the opportunity, working very closely with Sony and building that relationship. CTW: It’s interesting you should mention that. Is there any truth in the persistent rumour that Sony are highly displeased at your publishing of the official Xbox magazine? GI: I think if there was any truth, Sony would have expressed it publicly. The fact is we have a very robust relationship with Sony, we discuss with them at all stages what our business plans are, they know our financial position pretty well. They know what we’re doing and how we’re proceeding – we’ve been very careful to make sure there are very clear barriers between our Sony and Xbox magazines, just as I’m sure EMAP did when they had the official Sega and official Nintendo magazines. I would say, on a slightly more general point about gossip and so on, there’s inevitably a ton of speculation about our business. If you’re reading something on the Internet, inevitably there’s some degree of truth or speculation attached to it, and the fact is, it could as readily be a perfectly profound, detailed knowledge from an expert writing the comment, or it could be a disaffected former employee, or it could be someone in the middle of the night who’s got some angst for some reason, or whatever. There’s no hierarchy of information on the net, so you read something and you think "Well, it might be true". Well, indeed, it might be true. But there’s no greater reason for it to be true than if it was written by, you know, some gibbering fool in a cell. CTW: So I’m slightly confused now – is there any truth in the rumour about Sony being deeply hacked off about Official Xbox Mag or not? GI: Well, you’d have to address that question to Sony. But no, I don’t think so. I don’t think so. CTW: So how do you see the future? Hunkering down, concentrating on your core market of making videogames magazines, keeping away from the Internet until someone invents a profit model for it? Or just hanging on until someone sees a bargain and comes in and snaps up the whole company for peanuts? GI: This is a business which, historically, hasn’t spent very much money at all developing new magazines. What’s happened this year as much as anything else has taken us back to the philosophy that built the company, which is that we haven’t been major spenders of money, we’ve been creatures of niches and specialisms, and that is what we are as a business going forward. And so initially the main focus is going to be on games, because that’s where the greatest opportunity is over the next short time, but there will be other specialist-interest magazines, and we’ll just get on and do that and we’ll stand or fall on our ability to spot trends and compete well on them. And in that respect, it’s absolutely business as usual. I’m very very confident going forward that we’re going to look back and think "How on Earth was Future ever valued at thruppence?" That’s just an insane figure. As for a takeover, yes, we’re vulnerable. I don’t see a hostile bid coming in, but it’s something that could happen. It could happen today, tomorrow or never. We just have to wait and see. |

|

|

|

||

|

{kind=link}